Charitable Trust Asset Ownership Checker

The Bankruptcy

A trustee goes personal bankrupt.

Mission Impossible

The specific goal (e.g., curing a disease) is achieved or becomes impossible.

Donor Control

Founder wants to dictate investment decisions post-donation.

Personal Gain

Trustee sells assets to buy a luxury yacht.

Real Estate

Can the trust own land/buildings?

Private Trust Comparison

How does this differ from a private family trust?

You might assume that the people running a charity own its money, buildings, and equipment. It’s a natural assumption in a world where businesses belong to their shareholders. But when it comes to a charitable trust, which is a legal arrangement where trustees hold property for the benefit of others or for public purposes, the answer is surprisingly counterintuitive. No single person owns the assets of a charitable trust. Not the founder, not the board members, and certainly not the volunteers.

This distinction isn’t just legal jargon; it is the foundation of how charities operate, maintain accountability, and survive changes in leadership. If you are setting up a trust, serving as a trustee, or simply donating to one, understanding who actually holds the rights to these assets prevents costly mistakes and protects the mission you care about.

The Core Concept: Separation of Legal and Beneficial Title

To understand who owns what, we have to split the concept of "ownership" into two distinct parts. In common law systems, including New Zealand, the UK, and the US, property rights in a trust are divided between legal title and the right to control and manage the asset and beneficial interest, which is the right to enjoy the benefits of the asset.

In a standard private trust, like one set up to pay for your child’s education, the trustees hold the legal title, but your child holds the beneficial interest. They are the ones who get the money. However, a charitable trust is unique because it lacks specific, identifiable beneficiaries. You cannot point to a person and say, "This house belongs to Sarah." Instead, the beneficiary is the public or the community at large, or more specifically, the charitable purpose itself.

Because the "beneficiary" is an abstract concept (like poverty relief or animal welfare), the law treats the purpose as owning the beneficial interest. The trustees hold the legal title solely to execute that purpose. This means the assets are locked to the mission. A trustee cannot decide to sell the charity’s headquarters and buy a yacht, even if they legally sign the deed. The asset belongs to the cause, not the individual.

The Role of Trustees: Guardians, Not Owners

If no one owns the assets, who controls them? That responsibility falls on the trustees, who are individuals or organizations appointed to manage the trust's affairs in accordance with the trust deed. Think of trustees as professional guardians rather than owners. Their power is limited by the trust deed, which is the legal document establishing the trust and outlining its rules and objectives and by statute.

Trustees have a fiduciary duty. This is a high legal standard requiring them to act in the best interests of the trust, not themselves. They must avoid conflicts of interest, keep accurate records, and ensure every dollar spent advances the charitable purpose. In New Zealand, for example, the Charities Act 2005 sets out strict requirements for trustees to demonstrate that their actions align with the public benefit test.

Consider a scenario where a local environmental charity owns a plot of land used for tree planting. The trustees can decide to plant trees, hire staff, or lease part of the land for income. But they cannot sell the land to a developer unless the proceeds are strictly reinvested into similar environmental projects, and even then, they may need court approval if the sale deviates from the original intent. The land does not belong to the trustees; it belongs to the environment, held in custody by the trustees.

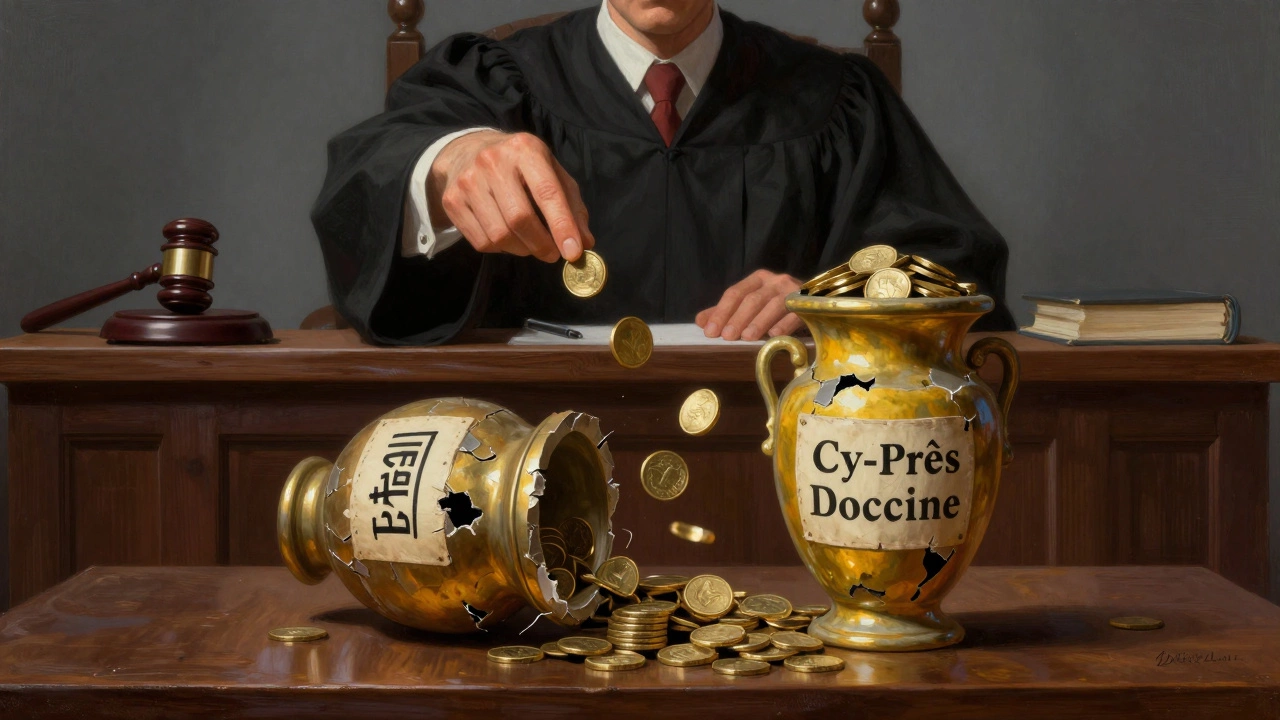

The Cy-Près Doctrine: What Happens When the Purpose Fails?

A common question arises when a charity’s goal becomes impossible to achieve. Maybe a trust was set up to support a specific school that has since closed, or a disease that has been cured. Who gets the leftover money? Does it go back to the donor? Do the trustees split it?

The answer is usually neither. This is where the cy-près doctrine, which is a legal principle allowing courts to redirect charitable funds to a similar purpose if the original one fails comes into play. "Cy-près" is French for "as near as possible." If the original purpose of the trust becomes impossible, illegal, or impractical, a court can order the assets to be transferred to another charity with a similar mission.

This doctrine reinforces the idea that the assets do not belong to the individuals involved. They belong to the charitable sector as a whole. For instance, if a trust dedicated to saving a specific species of bird finds that the species is extinct, the court will likely direct those funds to a general wildlife conservation group. The money stays within the ecosystem of charity, ensuring the donor’s initial intent of giving is honored, even if the specific target is gone.

Donors and the Illusion of Control

When you donate to a charitable trust, you often feel a sense of connection to how your money is used. Some donors try to insert clauses in the trust deed that give them ongoing control over investment decisions or hiring practices. While this is sometimes possible, it creates significant legal risks.

If a donor retains too much control, tax authorities may argue that the trust is not truly independent and therefore not eligible for tax-exempt status. The assets must be irrevocably given away. Once the donation is made, the donor loses all ownership rights. They become a stakeholder in the mission, but they have no claim to the balance sheet. This separation is crucial for maintaining the integrity of the charity. It ensures that the organization serves the public, not the whims of a wealthy benefactor.

Comparison of Ownership Models

| Entity Type | Legal Owner | Beneficial Owner | Can Assets Be Distributed to Individuals? |

|---|---|---|---|

| Private Company | Shareholders | Shareholders | Yes, via dividends or share sales |

| Private Trust | Trustees | Specific Beneficiaries | Yes, to named beneficiaries |

| Charitable Trust | Trustees (in name only) | The Public / Charitable Purpose | No, never to private individuals |

| Sole Proprietorship | Owner | Owner | Yes, entirely |

Practical Implications for Charity Management

Understanding that trustees do not own the assets changes how you manage risk. Since the assets are protected from personal claims, they are also protected from the personal debts of the trustees. If a trustee goes bankrupt, their creditors cannot seize the charity’s bank account. This separation provides stability for long-term projects.

However, it also means trustees must be diligent. Mismanagement of assets is not just a breach of contract; it can be a criminal offense in some jurisdictions. Trustees must ensure that investments are prudent and that insurance covers the physical assets. They must also keep clear records showing that every transaction serves the charitable purpose. Audits are not just bureaucratic hurdles; they are proof that the trustees are faithfully holding the assets for the public good.

For those looking to establish a charitable trust, clarity in the trust deed is essential. Vague language can lead to disputes later on. Specify the purpose clearly, define the powers of the trustees, and include mechanisms for changing the purpose if necessary, while adhering to local laws regarding cy-près applications.

Frequently Asked Questions

Can a trustee take money from a charitable trust for personal use?

No. Trustees are strictly prohibited from using trust assets for personal gain. Doing so is a breach of fiduciary duty and can result in legal action, removal from the board, and potential criminal charges depending on the jurisdiction. Trustees may be reimbursed for reasonable out-of-pocket expenses incurred while performing their duties, but they cannot draw a salary or profit unless explicitly allowed by the trust deed and approved by regulators.

What happens to the assets of a charitable trust if it closes down?

The assets cannot be distributed to the trustees or donors. They must be transferred to another registered charity with a similar purpose. This is often handled through the cy-près doctrine, where a court approves the transfer to ensure the funds continue to serve the public benefit. The trust deed may also specify a successor charity.

Does the founder of a charitable trust retain any ownership rights?

Generally, no. Once the assets are transferred to the trust, the founder relinquishes ownership. While founders can serve as trustees or directors, they hold the same legal responsibilities and limitations as any other trustee. Retaining excessive control can jeopardize the trust’s tax-exempt status.

Can a charitable trust own real estate?

Yes, a charitable trust can own real estate, such as office buildings, community centers, or land for conservation. The legal title is held by the trustees on behalf of the trust. The property must be used to further the charitable purpose, though it can be leased out if the income supports the mission.

Is there a difference between a charitable trust and a nonprofit company?

Yes. A charitable trust is governed by trust law and a trust deed, with trustees managing the assets. A nonprofit company (or incorporated society) is a separate legal entity governed by company law and a constitution, with directors managing the organization. Both serve charitable purposes, but their structures, liability protections, and governance rules differ significantly.